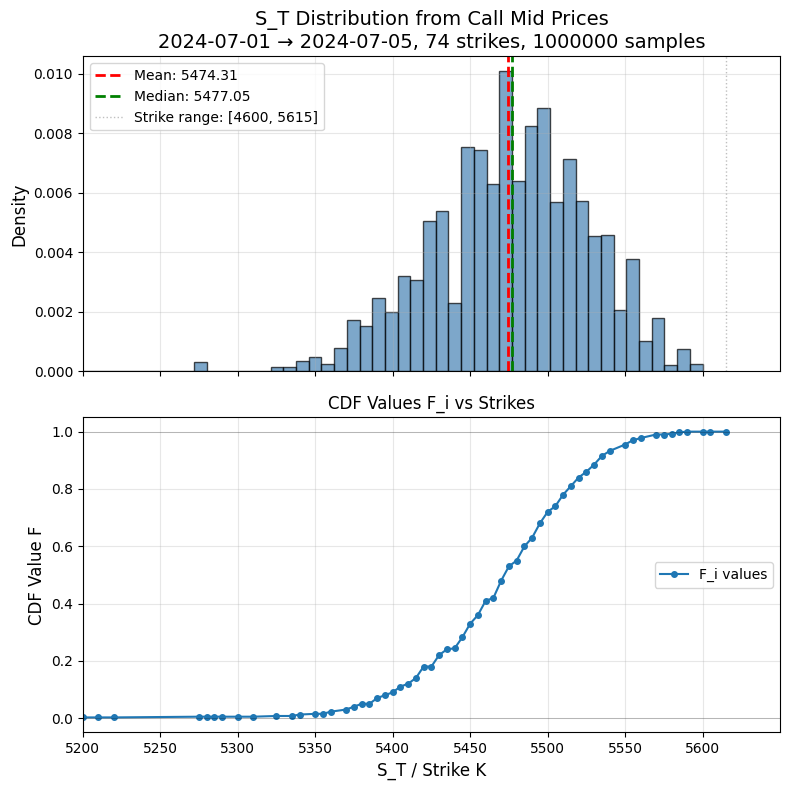

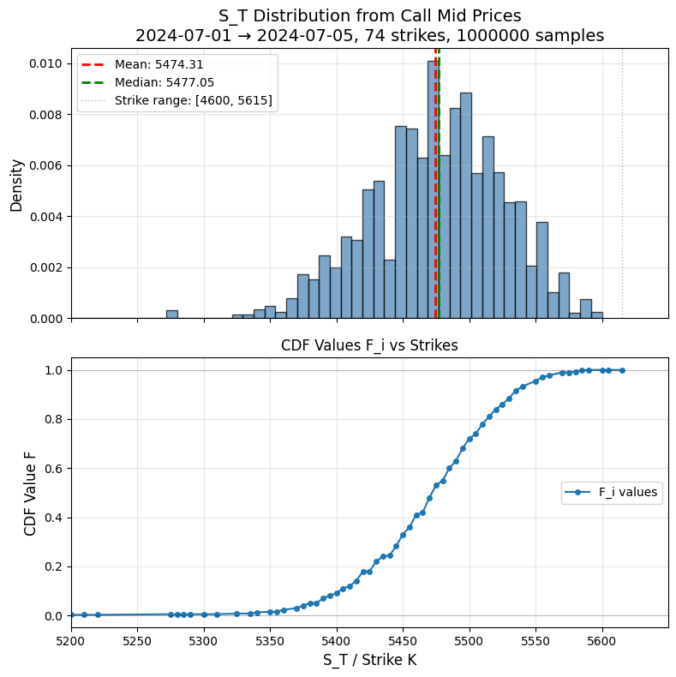

For a single maturity, European call prices encode the risk-neutral distribution of the underlying. You can turn them into Monte Carlo samples without fitting a model or estimating a density.

For strikes  with call prices

with call prices  , define

, define

![\[F_i = 1 + e^{rT} \frac{C_{i+1}-C_i}{K_{i+1}-K_i}, \quad F_0 = 0, \quad F_n = 1\]](https://www.sitmo.com/wp-content/ql-cache/quicklatex.com-67e0ef1fe3b0d34ac0811466d99b4ec6_l3.png "Rendered by QuickLaTeX.com")

This is a discrete approximation of the cumulative distribution function of  .

.

To sample:

- Draw

- Find

such that

such that

- Set

![\[S_T = K_i + (K_{i+1}-K_i)\frac{U-F_i}{F_{i+1}-F_i}\]](https://www.sitmo.com/wp-content/ql-cache/quicklatex.com-c33ca9b41ab9bb22d5436e82a1f3ef9e_l3.png "Rendered by QuickLaTeX.com")

Repeat for as many samples as needed.

This produces risk-neutral samples directly from observed call prices using only simple finite differences. It’s fully model-free, requires no volatility surface fitting, and preserves arbitrage constraints!

Below and example results from S&P500 option prices: